When a customer initiates a transfer, and the debit reflects the change, but the credit doesn't, you have a problem. Since there are thousands of users on payday, you risk triggering a fraud investigation before your engineering team manages to detect and fix the root cause. Software testing in a banking environment is all about providing you with the security coverage against any cases of non-compliance, or simply bugs that result in major financial losses. This guide gives your team a practical framework to learn the need for software testing in banking, based on your specific business scenarios.

Banking software failures cost millions and destroy customer trust. Rigorous testing is non-negotiable when handling transactions, sensitive data, and regulatory compliance that define financial services.

Critical Testing Areas for Banking

Security Testing – Validate encryption, penetration resistance, and protection against fraud and data breaches.

Transaction Accuracy – Ensure precise calculations for transfers, interest, fees, and currency conversions.

Compliance Validation – Test adherence to regulations like PCI DSS, GDPR, and financial reporting standards.

Performance Under Load – Verify system stability during peak transaction volumes and concurrent users.

Disaster Recovery – Validate backup systems, failover mechanisms, and data restoration procedures.

aqua cloud provides specialized testing capabilities for financial software with compliance tracking, security test templates, and audit-ready documentation. Banks using aqua reduce testing time by 50% while maintaining regulatory standards.

Banking software testing validates that financial applications calculate correctly, behave securely, and meet regulatory requirements. A bug in a game means replaying a level. A bug in banking means wrong account balances, exposed customer data, and a regulator asking questions.

Banking software testing is the validation of financial apps to ensure they’re functional and compliant with industry regulations. A defect in any regulated niche, where businesses are dealing with the finances of their customers, results in actual regulatory consequences.

At its core, banking software testing verifies three pillars:

Functional correctness. Does the system execute business rules accurately, including interest calculations, fee posting, payment routing, and ledger balancing?

Security and access control. Can the system withstand attacks, enforce authorization boundaries, and protect sensitive customer data?

Performance and resilience. Can it sustain peak loads, recover from partial failures, and meet the RTO/RPO objectives that regulators now formally assess?

Banking sits under a dense regulatory overlay: PCI DSS for card data, PSD2 for payments, GDPR for privacy, and DORA for ICT risk.

PSD2 for payment services, GDPR for data privacy, and DORA for ICT risk management. Each regulation introduces compliance testing practices that must be validated, documented, and proven to auditors.

Any banking software is highly regulated both locally and globally. That’s exactly why the quality of your testing directly impacts customer trust and compliance risks. Just as banking institutions require security measures, they need equally powerful test management solutions. This is where aqua cloud, an AI-powered test and requirement management platform, stands out. With aqua, financial institutions gain ISO 27001-certified and DORA-compliant test management that ensures every transaction, authentication flow, and calculation is thoroughly validated. Its domain-trained AI Copilot accelerates test case creation from requirements, generating project-specific test scenarios while maintaining complete audit trails. For banking teams juggling compliance needs and delivery pressure, aqua’s advanced reporting, that aggregated info from any connected software like Jira, provides real-time visibility into test coverage and defect status, which is essential for audits. aqua integrates natively with the tools banking QA teams already rely on, including Jira, Jenkins, Selenium, Playwright, Azure DevOps, and GitLab.

Boost your banking QA testing effectiveness by 80%

Compliant banking QA requires developers to apply multiple testing processes and frameworks. The main goal is to cover each risk vector. Basically, the notion is that no single approach, whether it’s only compliance or performance testing, or only a manual or automated one, is sufficient. A strong banking QA software helps to layer the following methods across the delivery lifecycle:

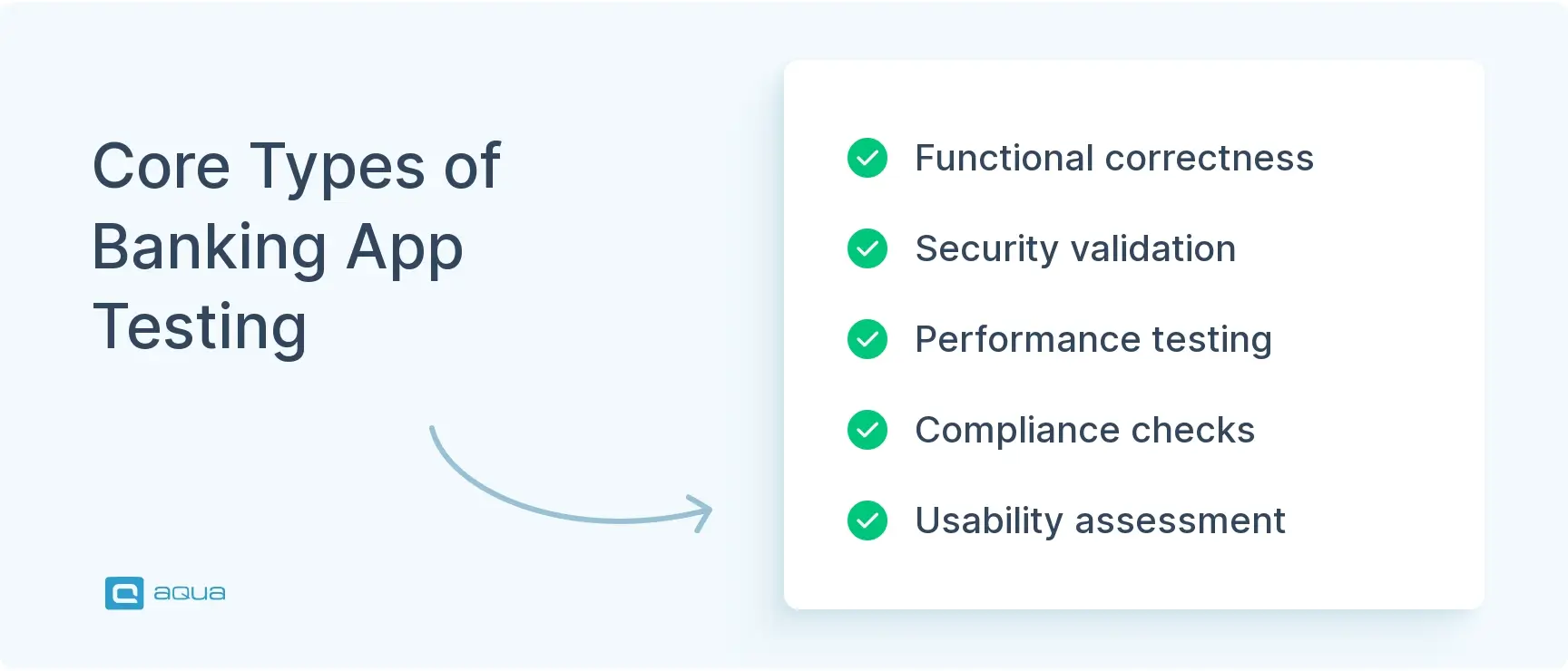

1. Functional testing

Functional testing validates that core banking operations follow defined business rules and calculate correctly. The question for your team is both whether a feature works and whether it calculates correctly under every condition your users will encounter.

Account opening, closure, and product migration logic

Interest and fee calculation across tiers and edge cases

Fund transfer debit/credit posting pairs and ledger balancing

Reversals, chargebacks, and refund processing

End-of-day cut-off handling and partial failure scenarios

2. Security testing

Security testing covers authentication flows, API endpoints, and business logic abuse across your banking systems. The OWASP API Security Top 10 is a standard reference your team should apply when running financial application testing against modern APIs.

Multi-factor and biometric authentication flows

Object-level and function-level authorization controls

Broken object-level authorization, excessive data exposure, rate limiting

Encryption protocols, secrets management, and PII logging hygiene

Threat-led penetration testing for DORA-scoped institutions

3. Performance testing

Performance testing confirms your systems handle payday spikes, month-end batch runs, and seasonal surges without degrading transaction integrity or customer experience.

Throughput and latency under concurrent user load

Batch window completion within defined time constraints

Queue backlog behavior and safe drainage after outages

p95/p99 latency measurement under stress conditions

Autoscaling validation and capacity threshold testing

4. Usability testing

Usability testing validates that your customer journeys are intuitive, accessible, and compliant with conduct risk expectations. Poor UX in banking drives support costs, increases abandonment, and can create regulatory exposure if customers make errors due to confusing interfaces.

Onboarding and KYC completion flows

Mobile and web payment journeys

SCA step-up prompts and fallback messaging

Accessibility compliance to WCAG standards

Error messaging accuracy and dispute initiation flows

5. Compliance testing

Compliance testing produces audit-ready evidence that your regulatory controls are implemented correctly and function as designed. Unlike functional testing, this discipline focuses specifically on what regulators and auditors will scrutinize during examinations.

SCA exemption logic under PSD2

Sanctions screening accuracy and AML rule validation

ISO 20022 message structure and field-level validation

PCI DSS segmentation boundary verification

Traceability from regulatory requirement to test execution evidence

Just use the fundamentals, these are some sample questions you can ask yourself. Also don’t make assumptions about the system.

Banking Industry-Specific Scenarios in Software Testing

If your institution has ever dealt with a failed payment batch or an authentication outage, you already know how quickly a software defect becomes a non-compliance case. The use cases below map to the failure modes that have triggered real fines and operational disruption across the industry, and each one shows where finance software testing directly intervenes.

1. Financial Correctness and Transaction Integrity

As a bank or payment processor, your systems must calculate and post financial values with complete precision. Interest accruals, fee applications, currency conversions, and ledger entries must balance perfectly across every account and every retry cycle. Errors in financial calculation aren’t isolated bugs; at scale, they become compliance incidents that your regulators will notice before your operations team does.

Relevant to:

Core banking and deposit accounting platforms

Loan origination and servicing systems

Payment processing and settlement engines

Treasury and general ledger systems

Subscription billing and recurring payment platforms

Software testing banking applications addresses financial correctness through property-based tests that assert fixed invariants:

Total debits must equal total credits

No account balance may change above its authorized transaction amount

Interest tiers must apply at exact configured thresholds

Idempotency tests simulate network retries to confirm the ledger rejects duplicate postings. Golden datasets validate calculation accuracy across product types. Batch testing verifies that end-of-day close completes within its window without leaving accounts in inconsistent states, even when a run fails mid-process and must restart.

2. Regulatory Compliance and Audit Readiness

If your institution operates under EBA, FCA, or ECB supervision, you already know how much weight regulators place on documented, traceable evidence of control testing. Overlapping frameworks like PCI DSS, PSD2, GDPR, DORA, and SWIFT CSP each carry specific, testable control requirements, and regulators assess both the quality of your testing and the traceability of its output.

Relevant to:

Retail and commercial banks under EBA, FCA, or ECB supervision

Payment institutions subject to PSD2 SCA requirements

Card issuers and acquirers in the PCI DSS scope

Institutions subject to DORA, which entered application in January 2025

Any firm processing EU personal data under GDPR

Every regulatory control needs a discrete, traceable test case your team can point to during an examination. SCA exemption logic requires tests for every exemption path, including low-value and trusted beneficiary flows, with step-up authentication validating correctly for high-risk transactions. PCI segmentation tests confirm CDE isolation, while DORA resilience tests validate RTO and RPO against defined objectives. Your test management platform must link each test to its regulatory requirement and preserve execution evidence. A timestamped audit trail needs to be available on demand. For a deeper look at what that process involves in the EU context, see this banking software testing audit guide.

3. Security Testing and Fraud Prevention

If you run a digital banking platform or open banking API, your systems are constantly targeted by fraud attempts, API abuse, and credential-based attacks. The controls sitting directly in your transaction path need to be tested with the same rigor you’d apply to any other critical system. Business logic flaws like bypassing velocity limits or manipulating beneficiary flows are just as dangerous as technical vulnerabilities. Standard scanning tools rarely catch them.

Relevant to:

Digital banking and mobile app platforms

Open banking API providers and TPP integrations

Card issuing, 3D Secure, and payment authorization systems

AML and fraud detection platforms

Identity and access management infrastructure

Security testing for your platform should work in layers. SAST and SCA catch vulnerable code and dependencies early in the pipeline, while DAST and API security tests validate runtime behavior against OWASP API Security Top 10 risks, covering broken object-level authorization and token scope violations. Penetration testing is mandated annually under PCI DSS and encouraged under DORA’s TLPT framework. It simulates real attacker behavior against your authentication flows and beneficiary management.

4. Payment Rail Integration and Cross-Border Processing

Cross-border payment processing means managing a chain of dependencies: domestic rails, SWIFT messaging, ISO 20022 transformation, sanctions screening, and FX conversion. A defect at any of those points can cause failed payments, compliance holds, or reconciliation breaks. By the time they surface in production, they’re expensive to get rid of.

Relevant to:

Correspondent banking and cross-border payment hubs

SEPA, Faster Payments, and domestic rail processors

Testing must validate the full message lifecycle from origination through to exception handling. ISO 20022 schema validation tests confirm correct MX field mapping and truncation prevention, which is critical as SWIFT’s coexistence period ends. Contract tests between your payment services and the ledger verify idempotency: retried payments must post exactly once. Sanctions screening regression suites should run on every ruleset update, using golden datasets of known-match and known-clean entities to confirm false negatives haven’t crept in through vendor-side logic changes.

Support payment integrations with comprehensive test management

5. Operational Resilience and Degraded-Mode Behavior

As a financial institution subject to DORA, you’re required to test digital operational resilience including your third-party ICT dependencies. The most damaging incidents are rarely full outages. Authentication slows down, a KYC vendor times out, queues start backing up. Systems that haven’t been tested under those conditions fail unsafely. A contained problem becomes a major incident.

Relevant to:

Cloud-hosted core banking and digital channel platforms

Multi-cloud financial market infrastructures

Payment processors with high-availability SLA obligations

Institutions subject to DORA operational resilience requirements

Any bank with material third-party ICT dependencies

Resilience testing for your environment needs to go above full-failover drills. Chaos engineering scenarios validate that your system degrades gracefully and recovers predictably, covering situations such as:

Authentication service latency injection

Database connection throttling

Third-party vendor outage simulation

DR drills must measure actual RTO and RPO against your documented objectives, not just confirm that failover occurred. DORA specifically requires that test outcomes are documented and reviewed at governance level, so your team needs a test management platform that can produce that evidence on demand.

6. Performance Under Peak Load and Batch Windows

Your banking platform faces predictable, extreme load events: paydays, month-end close, tax deadlines, and seasonal surges. Alongside these sit time-critical batch windows for interest accrual, regulatory reporting, and end-of-day ledger close. If your team hasn’t validated performance under these conditions, the first time you discover the limits of your system will be during a live incident.

Relevant to:

Retail banking platforms with high concurrent user volumes

Core banking engines running nightly batch close cycles

Regulatory reporting pipelines with hard submission deadlines

Data warehouses supporting real-time analytics

Performance testing must simulate realistic peak load profiles rather than average throughput. Payday scenarios combine login spikes with high-volume transfer initiation. Batch testing validates end-of-day close under production-representative data volumes, including DST transition dates and month-end boundary conditions. Beyond that, your tests must validate degraded-mode behavior: when load spikes, does your system queue transactions safely or start dropping them? p95/p99 latency measurements surface tail behavior that average metrics consistently mask.

7. Data Privacy, PII Handling, and Test Data Management

As a bank, you’re processing large volumes of sensitive personal and financial data every day, governed by GDPR and equivalent frameworks. The challenge extends into your test environments, which cannot use real customer data, yet synthetic data often misses the edge cases your validation depends on. Poor data hygiene in testing creates compliance exposure and coverage gaps at the same time.

Relevant to:

Any banking platform processing EU personal data under GDPR

KYC and identity verification systems handling biometric data

Analytics and data warehouse platforms with customer data feeds

Third-party vendors receiving data for testing or integration purposes

Observability and logging infrastructure with potential PII exposure

Your testing must confirm that PII does not leak into logs, APM traces, or analytics pipelines, since this is a common and costly failure mode in banking environments. Data masking pipelines need testing to confirm they consistently anonymize sensitive fields without breaking referential integrity. Synthetic data generation should be validated against production distributions to confirm it covers real-world edge cases. Don’t forget that role-based access controls should restrict even masked data to authorized testers.

8. Third-Party and Vendor Dependency Management

If your institution relies heavily on external vendors for KYC verification, sanctions data, OTP delivery, or payment processing, each of those relationships is a potential failure point. Supervisors assess third-party governance, and vendor changes can break your controls silently. Your testing programme needs to treat every vendor update as a potential regression risk.

Relevant to:

Banks using SaaS KYC or identity verification providers

Institutions dependent on cloud providers for critical ICT services

Payment firms relying on external OTP or authentication gateways

Compliance teams managing sanctions data vendor relationships

Any institution with material outsourcing arrangements under DORA

Contract testing defines the expected behavior of each vendor integration and automatically detects when vendor updates break that contract. Service virtualization simulates vendor outage scenarios, validating that your system queues safely rather than failing hard. Sanctions screening vendor updates must trigger automated regression suites before deployment. Above that, DORA’s concentration risk requirements mean your testing must cover exit scenarios: can your institution operate if a critical vendor becomes unavailable, and does the switchover actually work as documented?

Don’t be surprised if you have to automate for internet explorer too. Some banks apps still only work on IE.

The cost of improper banking QA is reflected in enforcement notices, incident post-mortems, and remediation budgets. Here are the exact consequences to keep in mind:

Regulatory fines and enforcement. TSB’s 2018 IT migration disaster, caused by insufficient testing and weak change management, resulted in a combined £48.65 million FCA/PRA fine and hundreds of millions in total incident costs, including customer redress and system remediation.

Financial crime control failures. Starling Bank received a £29 million FCA penalty for systemic weaknesses in financial crime controls, including inadequate screening coverage. Comprehensive AML and sanctions testing should have surfaced those defects before they reached production.

Operational and hidden costs. Except for fines, testing failures generate manual reconciliation backlogs, customer churn from eroded trust, and feature freezes during remediation. Opportunity cost compounds as delayed revenue accumulates.

Regulatory scrutiny of testing maturity. DORA mandates structured testing programmes for operational resilience, and examiners now evaluate whether firms test critical operations, validate third-party dependencies, and rehearse incident response as a formal control function.

Reputational damage. Rigorous banking software testing audit practices that prevent public incidents preserve the customer trust that takes years to build and very little time to lose.

Key Features of Banking Applications to Test

Banking applications bundle a distinct set of critical features, each carrying its own risk profile and regulatory implications. A strong test strategy maps these features to risk categories. This impacts both the appropriate test depth assigned and helps to extend test coverage to security, performance, and compliance.

1. Authentication and authorization gateways

Authentication is the entry point to your customers’ financial accounts, which makes it one of the highest-value targets in your system. Your testing must cover MFA flows, biometric enrollment and verification, device binding, and step-up authentication triggers under PSD2 SCA. Key edge cases include OTP delivery timeouts and whether session tokens can be manipulated to escalate privileges.

2. Account management

Account management covers opening, closure, dormancy, and product migration. Testing here focuses on fee accuracy, interest tier application at correct balance thresholds, and ledger integrity after closure. KYC/CDD validation must confirm that identity checks are complete before any account is activated, since gaps here create both compliance exposure and fraud risk.

3. Payment integration

Payment integration is where most high-severity defects appear, and where the consequences of a missed test case are felt immediately. Your testing must cover domestic and international payment rails, ISO 20022 message construction, idempotency under retries, and sanctions screening integration. Contract testing between payment services and ledger systems is particularly effective at catching integration defects early.

4. Card issuing and acquiring

Card environments fall under PCI DSS scope, which means vulnerability scanning, penetration testing, and segmentation validation are non-negotiable for your team. Test coverage must include card activation, PIN management, 3DS authorization flows, chargeback workflows, and fraud detection trigger logic such as velocity checks and geo-fencing rules.

5. Customer support channels

Chatbots, case management, and secure messaging all require testing for PII non-leakage in logs, authentication enforcement before sensitive operations, and accurate integration with fraud and complaints systems. If your customers can’t report fraud quickly, or if support staff can access account data they shouldn’t, you have a conduct risk problem that regulators will notice.

A mature test strategy maps cross-feature dependencies and tests the failure modes that span multiple systems at once, not just individual components in isolation.

Challenges in Banking Software Testing

Banking QA has a specific set of problems that most other software domains don’t encounter. These include the following:

1. Data privacy and test data scarcity

Your team cannot clone production databases due to GDPR and PII regulations, yet synthetic data often misses real-world edge cases such as orphaned accounts, legacy product codes, and unusual transaction patterns that only exist in live environments.

Solution: Invest in data masking pipelines, synthetic data generation tied to production distributions, and “golden customer” datasets. Test management platforms like aqua support role-based access controls that restrict even masked data to authorized testers, keeping privacy compliance intact throughout the test lifecycle.

2. Complex integrations and environment fragility

A single customer journey may touch ten microservices, multiple external vendors, a legacy core, and a data warehouse. Test failures frequently stem from environment issues rather than application defects, generating noise and eroding confidence in your automation results.

Solution: Layer contract tests for integration points with isolated service tests using service virtualization, plus a minimal suite of stable end-to-end tests. Test management tooling should clearly distinguish environment failures from application failures in reporting, so false signals don’t flood your defect queues.

3. Shifting regulatory requirements

ISO 20022 migration timelines, PSD2 updates, DORA deadlines, and PCI DSS v4.0 changes mean your test suites need continuous maintenance. Compliance testing reflects current regulatory interpretation, not a one-time snapshot.

Solution: Tag test cases by regulation and link them to specific control requirements in a test management platform. When a regulatory update arrives, impact analysis identifies which suites need updating, and audit trails show regulators that your programme reflects current requirements.

4. Degraded-mode and partial failure scenarios

Most real incidents are partial failures rather than complete outages. Authentication runs slow, a KYC vendor times out, queues backlog. Systems that haven’t been tested under these conditions fail unsafely and turn contained problems into major incidents.

Solution: Build chaos engineering practices into the standard regression suite using controlled fault injection. Test management platforms should track resilience drill outcomes with the same rigor as functional test results, giving governance-level visibility into your operational readiness.

Best Practices for Banking Software Testing

The practices below reflect what works in institutions providing financial services testing:

1. Start with risk-based prioritization. Begin by mapping your critical customer journeys, including login, payments, sanctions screening, and end-of-day close, to their system dependencies. From there, assign test depth proportional to the regulatory and financial impact of failure, so high-risk areas get deeper coverage and more frequent testing cycles.

2. Build compliance traceability from day one. Link regulatory requirements to user stories, test cases, execution results, and defect records in a dedicated test management platform. When an examiner asks how your team validated SCA exemptions, you produce a timestamped audit trail rather than a spreadsheet assembled under deadline pressure.

3. Automate at the right layer. Prioritize unit tests for financial rules, contract tests for service integrations, and a small suite of stable critical-journey end-to-end tests. Over-investing in UI automation consumes your maintenance budget without improving defect detection. For a broader view of which testing types for financial apps deliver the best signal at each layer, see our dedicated guide.

4. Embed security throughout delivery. Integrate SAST, DAST, and SCA into the CI/CD pipeline so security validation runs on every build, and include API security tests targeting OWASP risks as part of every deployment.

5. Rehearse resilience with measurable objectives. DR drills and chaos experiments need pass/fail criteria tied to RTO/RPO targets. DORA expects evidence that resilience testing outcomes were reviewed at governance level, making documentation of drill results a regulatory requirement. For a review of the best test management for banking that can support this end-to-end, see our comparison guide.

Emerging Trends in Banking Application Testing

Bank software testing is changing fast. Staying ahead of the following shifts gives your team a real advantage, both in quality outcomes and in the evidence you can produce for regulators:

AI-powered test generation. Tools, such as a [free AI test case generator] by aqua(https://aqua-cloud.io/free-ai-test-case-generator/), can now analyze application behavior. This allows, for example, to surface high-risk tests and generate edge case scenarios automatically. With such instruments, your team spends less time on repetitive case writing and more on the scenarios that matter. Google’s testing blog covers practical applications at scale.

RegTech for compliance automation. Platforms now parse ISO 20022 message schemas and auto-generate validation test cases. Some solutions also monitor updates from bodies like the EBA and SWIFT CSP, flagging impacted test suites before your team has to manually track them down.

Shift-left security. Embedding SAST, SCA, and API contract security validation into every delivery stage catches vulnerabilities when they’re cheapest to fix. The OWASP DevSecOps Guideline provides a practical framework for your team, and the approach aligns with DORA and FFIEC IT Handbook expectations around secure SDLC practices.

Chaos engineering for operational resilience. Controlled fault injection has moved from experimental to a supervisory expectation under DORA. Tools like Gremlin and Chaos Mesh make resilience experiments accessible at scale, and pairing them with observability platforms lets your team validate that incident response playbooks hold up under realistic pressure.

Biometric and behavioral analytics testing. As your institution moves beyond password authentication, testing now covers fingerprint matching accuracy, facial recognition false accept/reject rates, and liveness detection. Bias validation matters here too, since authentication models that disadvantage specific demographics create both conduct risk and EU AI Act exposure for high-risk AI systems.

Some of these are already showing up in supervisory expectations: DORA’s engineering requirements are the clearest example.

The question wiith banking software testing is how to do it efficiently while maintaining the standards that regulators and customers demand. aqua cloud, and AI-driven test and requirement management platform, delivers what banking QA teams need: a secure, compliance-focused QA environment that accelerates testing without compromising quality. Its domain-trained AI Copilot creates context-aware scenarios grounded in your banking application’s specific requirements and documentation. With granular role-based access control, comprehensive audit trails, and seamless integration with your existing DevOps toolchain, aqua streamlines the entire testing lifecycle while maintaining the security posture financial institutions require. aqua connects out of the box with Jira, Jenkins, Selenium, Playwright, Azure DevOps, GitLab, and your broader CI/CD ecosystem via REST APIs. This provides your banking teams with a unified compliance and quality hub without replacing the tools your engineers already depend on.

Save 12.8 hours per tester per week with aqua’s AI

Software testing for banking applications is what provides your operational resilience and under the regulatory exposure. Every fund transfer, authentication flow, and interest calculation your systems process carries financial and reputational weight that demands rigorous validation. Institutions that treat testing as a strategic investment consistently are the ones that undergo regulatory examinations without incidents. Let the testing right, and your systems handle whatever comes at them. Get it wrong, and the consequences show up in your incident log, your audit report, or both.

How is security testing performed to protect sensitive banking data?

Security testing in banking layers SAST, DAST, SCA, and penetration testing across the delivery lifecycle. API tests target OWASP Top 10 risks. PCI DSS mandates annual pen tests, and DORA encourages threat-led penetration testing for critical institutions. All findings must be tracked, retested, and evidenced for audit.

What challenges are unique to automation testing in banking applications?

Banking automation faces data privacy constraints that prevent use of production data in test environments, complex multi-vendor environment fragility, and regulatory traceability requirements that mandate evidence capture alongside execution. Time-dependent batch jobs and compliance-linked test suites add layers of complexity that most other software domains don’t encounter.

What is DORA and how does it affect banking software testing?

DORA, the Digital Operational Resilience Act, entered application in January 2025 and requires EU financial entities to maintain structured ICT testing programmes. This includes resilience testing of critical services and third-party dependencies. For critical institutions, DORA also encourages threat-led penetration testing with documented, governance-reviewed outcomes.

How do banks manage test data without violating GDPR?

Banks use data masking pipelines to anonymize production data, synthetic data generation tools to create realistic test datasets, and tokenization strategies that preserve referential integrity without exposing PII. “Golden customer” datasets cover key edge cases. Test management platforms enforce role-based access to ensure even masked environments stay compliant.

Home » Best practices » Banking & Financial Software Testing: Ultimate Guide

Do you love testing as we do?

Join our community of enthusiastic experts! Get new posts from the aqua blog directly in your inbox. QA trends, community discussion overviews, insightful tips — you’ll love it!

We're committed to your privacy. Aqua uses the information you provide to us to contact you about our relevant content, products, and services. You may unsubscribe from these communications at any time. For more information, check out our Privacy policy.

X

🤖 Exciting new updates to aqua AI Assistant are now available! 🎉