How to Automate Testing for Fintech Apps: Tools, Process & Strategy

When your software deals with customers’ financial and personal data, all the defects carry financial and legal risks. Most fintech failures are underneath the UI, in backend logic and third-party integrations your QA team oftentimes can’t test fully manually. No wonder you are extensively using automated testing, are you? Keeping test scripts current with changing compliance requirements is a challenge of its own. This guide covers how to build automated testing for fintech apps, from the types of tests your team needs to the tools, process steps, and practices that produce audit-ready results.

Automated testing in fintech validates transaction accuracy, ledger logic, encryption behavior, compliance controls, and API resilience. UI correctness is one layer among several.

DORA, effective January 17, 2025, requires EU financial entities to test ICT resilience, incident recovery, and third-party risk as part of mandatory operational requirements.

Test automation should run SAST, SCA, DAST, secret scanning, and container checks in CI/CD pipelines, not rely on annual penetration tests that leave vulnerabilities undetected for months.

Fintech test suites need layered coverage across unit, API, contract, E2E, security, performance, and compliance tests.

AI-assisted QA tools can support test generation and maintenance, but only 15% of organizations have scaled GenAI in QA enterprise-wide.

See how to build an automated testing strategy for your best fintech application 👇

What Is Automated Testing in Financial Technology?

Automated testing for fintech apps means using code to validate that financial software behaves correctly, securely, and reliably across the scenarios that matter. Instead of manually clicking through payment flows or simulating failed transactions on every push, you write tests that handle this work automatically. These tests run on every commit, catch regressions before they reach production, and document that critical flows work after each update.

Fintech test automation covers behavior that UI checks can’t reach: double-entry ledger logic, currency rounding precision, role-based access controls, webhook idempotency, and audit trail completeness. A mature fintech test suite validates outcomes across multiple layers. Unit tests cover business logic and feed into integration tests that handle third-party banking APIs. Contract tests verify open banking integrations, while E2E tests validate core user journeys like onboarding, KYC verification, and wallet top-ups. Each layer exposes different failure modes, and you need all of them.

The environment your tests operate in makes fintech different from standard SaaS testing. Your apps handle sensitive personal data, real-time transactions, fraud detection engines, and third-party integrations that fail unpredictably. The test suite needs to prove that controls exist, that failures are handled gracefully, and that your system holds up under audit scrutiny.

When DORA came into force in the EU on January 17, 2025, it made ICT risk management and digital operational resilience mandatory for financial entities. Testing became part of governance. The next section explains why that matters.

Why Automated Testing Is Critical for Fintech

One bug in production can mean a regulatory fine, a data breach, or money out of customer accounts. A typo in a social media app is a bad day. In a payment app it has legal consequences.

Security vulnerabilities found in CI/CD cost far less to fix than ones found post-breach. Running SAST, DAST, SCA, and secret scanning against OWASP Top 10 for 2025 catches problems months before a penetration test would. Automated tests also produce timestamped evidence that access controls, audit logs, MFA checks, and data retention rules actually work — which is what regulators want to see. And unlike manual testing, automated regression suites scale with your product without adding headcount.

Security flaws are expensive: Running SAST, DAST, SCA, and secret scanning in CI/CD catches vulnerabilities months before a once-a-year penetration test would, using OWASP Top 10 for 2025 standards as the baseline.

Compliance requires proof: Automated tests generate consistent, timestamped evidence that access controls, audit logs, MFA checks, and data retention rules function correctly, giving regulators something concrete to review.

Manual testing doesn’t scale: Automated regression suites keep pace with new features, integrations, and edge cases without adding QA headcount or slowing your release cycle.

Third-party integrations break often: Contract tests, API mocks, and retry logic validation catch payment gateway and bank API failures before customers encounter them in production.

Performance failures are difficult to detect: Load tests expose latency, timeout, and throughput issues under realistic traffic conditions before salary days or market events trigger them in production.

These factors explain why automated testing in fintech is core infrastructure. The next section covers the regulatory side in detail.

When you’re building test automation for fintech, writing the tests is where the work just gets up and running. You also need to maintain traceability across releases and produce audit-ready evidence on every deployment. That’s where aqua cloud, an AI-driven test and requirement management platform, fits in as core infrastructure. With aqua, you get end-to-end traceability from requirements through test execution to defect resolution. Automated audit trails timestamp every action, and compliance workflows align with ISO 27001, DORA, and financial regulations. The AI Copilot uses RAG grounding and learns from your uploaded documentation, whether internal compliance policies, API contracts, or security standards. Generated test cases stay contextually accurate and project-specific, grounded in your actual requirements. Compliance reports hold up under regulatory review, execution automates through your existing CI/CD setup, and test results stay linked directly to the requirements they cover. aqua connects natively with Jira (bidirectional sync), Jenkins, Azure DevOps, Confluence, SoapUI, and Ranorex.

Build audit-ready fintech test automation with full traceability and compliance in one platform

If you’re building fintech software, you’re building under regulatory oversight. The rules vary by region and product type, but the core principle is the same: prove your system handles money and data safely. Automated testing produces that proof by showing controls work consistently across releases.

Here are the key regulatory areas where automation plays a role:

DORA (Digital Operational Resilience Act)

Effective January 17, 2025, for EU financial entities. DORA covers:

ICT risk management

Incident reporting

Operational resilience

Third-party risk

Testing is explicitly part of the framework. You’re expected to validate resilience, recovery, and continuity under stress. Automated tests for incident simulation, failover logic, and service degradation help satisfy these requirements.

PCI DSS v4.0.1

Applies if your app processes, stores, or transmits payment card data. The PCI Security Standards Council maintains v4.0.1 as the current standard.

Automated tests can validate:

Encryption and tokenization

Session timeout and access logging

Secure transmission practices

Automation doesn’t replace formal PCI audits. It proves controls function between assessments.

GDPR and Data Protection

Fintech apps collect personal data. For EU users, GDPR compliance is non-negotiable. Automated tests should cover consent tracking, data retention rules, deletion workflows, and access controls.

For example: a test can confirm that user data is anonymized after account closure, or that export requests return complete datasets.

OWASP Standards

OWASP provides security baselines that regulators and auditors frequently reference:

OWASP MASVS — mobile fintech apps, covering authentication, cryptography, local storage, network communication, and platform interaction

Open Banking and FAPI

Building open banking features? FAPI matters. The OpenID Foundation announced FAPI 2.0 Security Profile as a final specification in February 2025, with conformance tests available in July 2025.

Automated API tests can verify token handling, consent workflows, and secure communication channels required by FAPI.

AML and KYC Regulations

Anti-money laundering and know-your-customer rules require identity verification, risk scoring, and transaction monitoring. Automated tests should cover:

KYC status checks

Document validation workflows

AML flag triggers

High-risk transaction scenarios

These tests don’t replace manual review. They prove the logic functions as designed.

The common thread across all these requirements is traceability. Your automated tests should link to the control they validate, produce evidence that it works, and store that evidence for audit purposes. A well-designed test report shows what was tested, when it ran, which environment it ran in, and what passed or failed. That documentation becomes your compliance paper trail when auditors arrive.

Main Challenges in Testing Fintech Applications

Building a strong test suite for fintech software is harder than it looks. The usual automation challenges, such as flaky tests, environment instability, and maintenance overhead, still apply. Fintech adds layers of complexity that most QA teams don’t encounter elsewhere. Here’s what makes it difficult:

Ledger and Balance Accuracy: UI tests can confirm the displayed balance looks correct, but they won’t validate backend accounting logic. Your team needs to check double-entry ledger consistency, pending vs. settled transaction states, refund handling, currency rounding, fee calculations, and reconciliation records. If the UI shows $100 but the ledger records $99.99, top-level tests won’t catch it.Solution: Write dedicated ledger tests that query the database directly after each transaction, verifying balance, fees, and reconciliation records against expected values. Run these on every commit alongside your functional suite.

Third-Party Integration Instability: Fintech apps depend on payment gateways, bank APIs, KYC providers, fraud engines, and notification services. These integrations time out, change contracts, return unexpected error codes, or go down entirely. Testing these flows requires mocking, contract testing, retry logic validation, and fallback scenario coverage, all of which add complexity to your test suite.Solution: Use WireMock or Mountebank to simulate payment gateway and bank API responses, including timeouts and error codes. Run contract tests against real provider schemas to catch breaking changes before they reach production.

Sensitive Test Data Management: You can’t use real customer data or payment credentials in test environments, but you need realistic data to catch edge cases. Generating synthetic test data for users, accounts, transactions, cards, KYC documents, and risk profiles takes time. You also need to ensure test data doesn’t leak into logs, screenshots, or error messages.Solution: Build a synthetic data generator that produces realistic users, accounts, and transactions with anonymized identifiers. Enforce log masking and access controls so test credentials never appear in error messages or screenshots.

Regulatory Audit Requirements: Tests serve as compliance evidence as much as they catch bugs. That means every automated test needs traceability to requirements, clear pass/fail criteria, environment details, and result storage. Building this documentation layer without slowing down your release cycle is tricky.Solution: Tag every test case with the requirement or control it validates and configure your test management tool to export timestamped reports. That output becomes your audit evidence without extra manual documentation work.

High-Risk Edge Cases: Most fintech bugs appear in edge cases such as expired sessions, declined payments, duplicate webhooks, insufficient funds, blocked accounts, chargebacks, and fraud flags. These scenarios are harder to automate because they require specific system states, third-party responses, or timing conditions that don’t exist in normal happy-path flows.Solution: Build a dedicated edge case library covering declined payments, duplicate webhooks, expired sessions, and provider timeouts. Use test data factories to create the specific account states these scenarios require to execute reliably.

Security Testing Gaps: Running a penetration test once a year leaves too much exposure between checks. Automated security checks, including SAST, SCA, DAST, and secret scanning, should run in CI/CD. These tools generate false positives, require tuning, and don’t cover logic or business logic vulnerabilities. Your team needs both automation and human review.Solution: Integrate SAST, SCA, secret scanning, and DAST into your CI/CD pipeline as mandatory stages with blocking thresholds. Assign ownership for triage so findings get addressed within each sprint instead of stacking up in a backlog.

Performance Under Load: Payment spikes happen during salary days, market events, or sales campaigns. Load testing for fintech apps means simulating concurrent transactions, API throughput, database query performance, queue processing, and webhook delivery volume. Performance tests require dedicated infrastructure, realistic data volumes, and careful analysis of latency and error rate patterns.Solution: Run load tests in a staging environment with production-mirrored data using JMeter or k6 to simulate peak traffic scenarios. Set explicit SLA thresholds and fail the pipeline build if response times exceed them.

These challenges explain why many fintech teams struggle to scale their test automation. The next section breaks down the types of tests you need to address them.

Types of Automated Testing for Fintech Apps

A strong test automation strategy for fintech apps is built on layers. Each layer catches different failure modes, and you need all of them to cover functional correctness, security, performance, compliance, and operational resilience.

Unit Tests

Unit tests validate isolated business logic functions in complete isolation from external dependencies, running on every commit to catch calculation and validation errors at the source.

Cover:

Fee calculations, interest formulas, and currency conversion logic

Risk scoring rules and input validation constraints

Date handling, repayment schedule calculations, and rounding behavior

Field-level validation and sanitization logic

Integration Tests

Integration tests verify that your services, databases, queues, and external APIs communicate correctly, covering the data flow between components that unit tests can’t reach.

Cover:

Payment provider request handling and error response propagation

Bank API communication and retry behavior on failure

Webhook ingestion, message queue processing, and consumer acknowledgment

Data synchronization between services and fallback behavior on timeout

Contract Tests

Contract tests verify that a service consumer and provider agree on request and response structures, catching breaking API changes before they reach integration or E2E layers.

Cover:

API schemas, field types, and status codes for internal microservices

Payment gateway and bank API contract agreements

Open banking API structures and KYC vendor payload formats

Notification service payload schemas and versioning expectations

API Tests

API tests validate the full behavior of your endpoints beyond schema correctness, covering authentication, authorization, and edge case handling at the transport layer.

Cover:

Authentication flows, token validation, and authorization rule enforcement

Rate limit behavior, idempotency keys, and duplicate request handling

Negative tests for malformed payloads, missing fields, and invalid tokens

Backward compatibility checks across API versions

End-to-End (E2E) Tests

E2E tests validate complete user journeys across the full application stack, proving that critical business flows work correctly from the user’s first action to the final database state.

Cover:

Onboarding with KYC activation and account creation confirmation

Wallet top-up with real-time balance update and notification delivery

Card payment with 3DS challenge, transaction history, and ledger entry

Bank transfer with confirmation notification and audit log creation

Failed payment with retry logic, error state, and audit trail entry

Security Tests

Security tests validate that your application resists known attack vectors, with automated checks running in CI/CD to catch vulnerabilities before they reach staging or production. Use OWASP standards as your baseline.

Cover:

SAST for source code vulnerabilities and SCA for dependency risks

Secret scanning and container image checks on every build

DAST and API fuzz testing for runtime attack surface exposure

Access control validation and privilege escalation scenario testing

Performance and Load Tests

Performance tests validate that your application meets latency and throughput targets under realistic and peak traffic conditions, exposing bottlenecks that only appear at scale. For real-time payments like FedNow, latency and availability expectations are especially demanding.

Cover:

Concurrent transaction throughput and API response latency under load

Database query performance against production-scale data volumes

Queue processing time and webhook delivery rate at peak volume

Recovery time after traffic spikes and service restarts

Mobile Security Tests

Mobile security tests validate the security controls specific to iOS and Android fintech apps, covering authentication, local storage, and platform-level attack surfaces. Align with OWASP MASVS and MASTG.

Cover:

Biometric login, device binding, and session timeout enforcement

Jailbreak and root detection under real-device conditions

Secure local storage validation and data leakage through logs or screenshots

Deep link handling, app backgrounding, and OS version compatibility

Compliance and Audit Tests

Compliance tests verify that your application’s controls function consistently and produce the evidence regulators expect, linking automated test results to specific requirements.

Cover:

Access control enforcement and role-based permission validation

Audit log completeness, timestamp accuracy, and tamper detection

Data retention rules, consent tracking, and deletion workflow correctness

MFA enforcement and PCI-related cardholder data handling

Data and Ledger Tests

Ledger tests validate the accounting accuracy of every transaction at the database level, going beyond what the UI displays to verify that backend records are complete and consistent.

Cover:

Double-entry ledger consistency after payments, refunds, and reversals

Pending vs. settled transaction state transitions and timing accuracy

Currency rounding, fee calculation, and chargeback record handling

Reconciliation record completeness and transaction history accuracy

Each of these test types plays a specific role in your overall quality strategy. The next section walks through the automated testing process step by step.

Currently using a mix of automated unit tests I built myself and a part-time QA person for the edge cases that always break payment flows. Would definitely consider a specialized service if the pricing made sense - probably looking at like $500-1k/month range for comprehensive coverage

The Automated Testing Process for Fintech Apps: Step-by-Step

Automated testing in QA for fintech is an array of procedures to set up the system, starting from requirements and risks up to integration of AI. All should be done with consideration of fintech-specific factors like dealing with customers’ sensitive private and financial data. Here’s how to structure that process from start to finish:

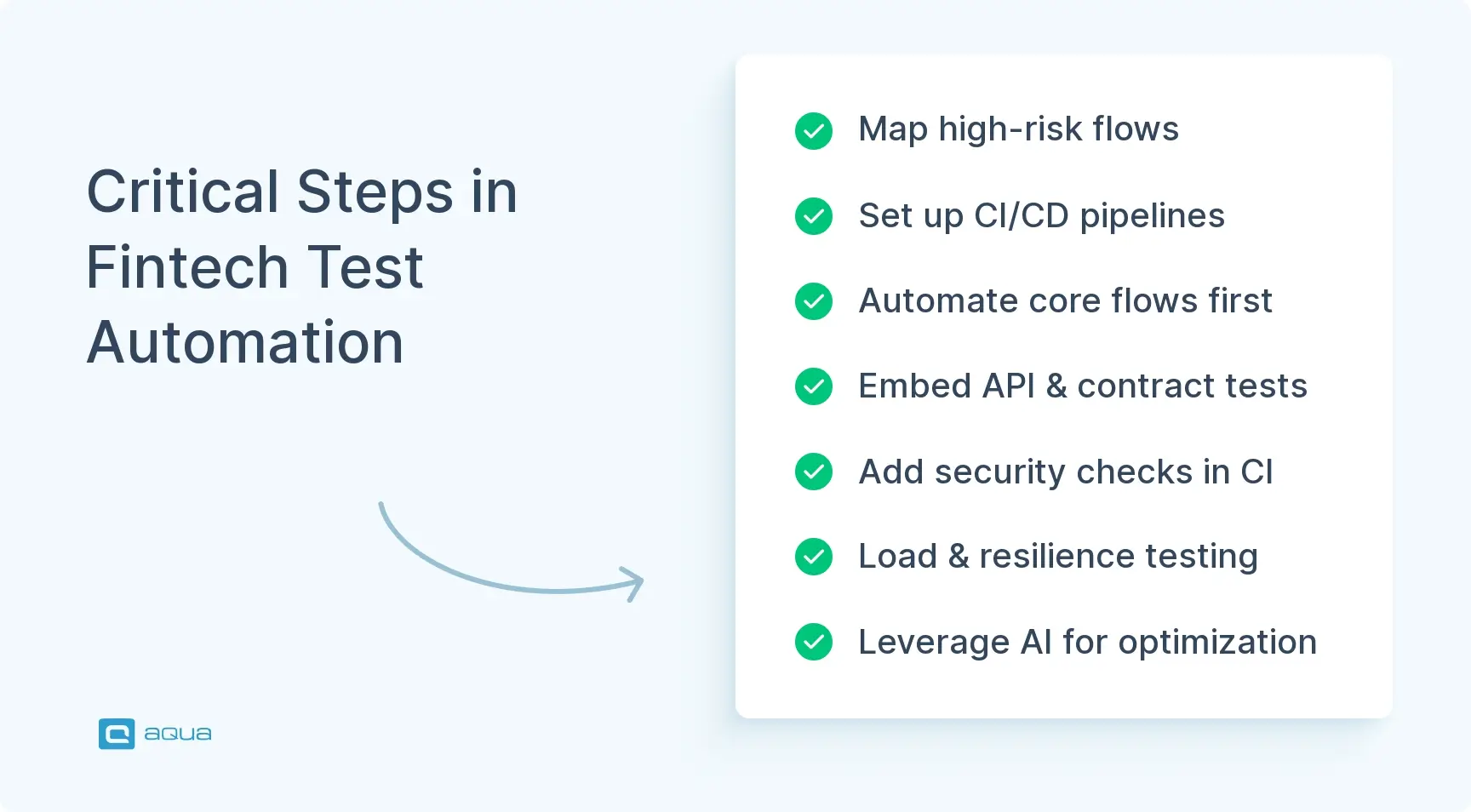

Step 1: Risk Mapping: Identify the highest-risk flows: money movement, authentication, KYC, card data handling, personal data storage, regulatory reporting, fraud detection, admin permissions, and third-party integrations. Map these risks to features, rank them by impact and likelihood, and use that ranking to prioritize your automation backlog.

Step 2: Foundation Setup: Set up test environments, CI/CD pipelines, reporting dashboards, test data generation, and automation standards. Define coding conventions, test structure guidelines, and documentation requirements. Choose your framework, set up version control, and integrate test execution into your build pipeline.

Step 3: Core Regression Automation: Automate the most stable and business-critical flows first: login and MFA, onboarding, KYC status, wallet top-up, transfer, refund, failed payment, admin block/unblock, and audit log validation. These tests form your smoke and regression suite, running on every pull request and deployment.

Step 4: API and Contract Testing: Add API-level validation and contract testing for internal and external integrations. Build an API regression suite, define your provider mock strategy, write contract tests for payment gateways and bank APIs, and validate webhook test coverage. This layer catches integration issues before they reach E2E tests.

Step 5: Security and Compliance Automation: Embed security checks into CI/CD: SAST, SCA, DAST, secret scanning, container scanning, and API security tests. Add OWASP-based checks, PCI-related validation where relevant, and access control test suites. Configure reporting to capture audit evidence for compliance purposes.

Step 6: Performance and Resilience Testing: Add load, stress, endurance, and failover tests. Establish performance baselines, validate SLA/SLO targets, simulate incidents, and track resilience test results. Run these tests in staging or production-like environments to get realistic measurements.

Step 7: AI-Assisted Optimization: Use AI tools to support test design, test maintenance, duplicate detection, defect clustering, and coverage gap analysis. According to Capgemini’s World Quality Report 2025–26, 43% of organizations are experimenting with GenAI in QA, but only 15% have scaled it enterprise-wide. Apply AI with human review, traceability rules, and governance policies to avoid introducing blind spots.

This process should be iterative. Start with the highest-risk areas, build your foundation, expand coverage incrementally, and refine your strategy as your product evolves. The next section covers the tools you’ll need to execute this process effectively.

Popular Tools for Fintech Test Automation

Choosing the right tools depends on your product architecture, team skills, compliance requirements, and release model. Here are the most commonly used tools for fintech test automation, broken down by category:

Test Management and Requirements Traceability

Test and requirement management platforms keep requirements, test cases, and results in a single traceable chain. That’s especially convenient for regulated industries. Gaps or missing timestamps cast doubt on whether there’s a suitable automated testing control in place. A unified platform minimizes non-compliance risks.

aqua cloud sits at this intersection. It was designed for software teams in regulated industries where traceability is a compliance requirement, taking a different approach from general-purpose tools that were built for agile velocity and later adapted for compliance reporting. aqua built the audit trail as a core concern from the start. Requirements live alongside test cases, test runs link back to the requirements they cover, and defects close the loop. All of it is timestamped and versioned, so evidence is always export-ready. aqua holds ISO 27001 certification and has been adopted by financial services teams working under DORA and PCI DSS, which reflects its fit in environments where every control needs documented proof.

Boost the efficiency of your automated testing for fintech by 80%

Zephyr Scale for Jira-native test case management with coverage traceability

qTest for enterprise test management with CI/CD reporting integration

TestRail for structured test case management and milestone-based coverage reporting

Allure for open-source test result reporting and trend visualization

API Testing Tools

API testing is critical for fintech because most financial logic lives at the API layer, making this category essential for validating payment flows, authentication, and third-party integrations.

Postman for API testing, monitoring, and collection-based regression suites

REST Assured for Java-based API automation within existing test frameworks

Karate DSL for combined API and UI testing in a single framework

Pact for consumer-driven contract testing across internal and external APIs

Contract Testing Tools

Contract tests prevent integration failures by verifying that API producers and consumers agree on request and response structures before code reaches staging.

Pact for consumer-driven contract tests with provider verification

Spring Cloud Contract for contract testing within Spring-based microservices

Postman Mock Server for simulating provider responses during consumer development

UI and E2E Testing Tools

Use UI tests sparingly and focus them on the critical journeys that require full browser rendering to validate correctly.

Playwright for modern multi-browser testing with fast parallel execution

Cypress for developer-friendly testing with fast local feedback loops

Selenium for broad browser support across legacy and modern environments

Appium for mobile cross-platform E2E coverage on iOS and Android

Mobile Testing Tools

For mobile security, align your framework choices with OWASP MASVS and MASTG standards.

Appium for cross-platform mobile automation on real devices and emulators

XCUITest for native iOS UI and integration testing

Espresso for native Android UI testing with tight Gradle integration

BrowserStack or Sauce Labs for cloud device farm access across real devices

Security Testing Tools

Security checks should run in CI/CD on every build, with findings treated as pipeline blockers rather than backlog items.

SonarQube for SAST and code quality analysis across commits

Snyk for SCA with dependency vulnerability detection and fix suggestions

OWASP ZAP for DAST and API security scanning in automated pipelines

GitGuardian or Gitleaks for secret scanning across commits and branches

Trivy for container image scanning and infrastructure-as-code checks

Burp Suite for both manual security testing and automated API scanning

Performance Testing Tools

Performance testing in fintech should simulate realistic transaction volumes, concurrent users, and third-party API latency to expose issues before they appear in production.

JMeter for load testing with broad protocol support and detailed reporting

Gatling for high-throughput load simulation with Scala-based scripting

k6 for developer-friendly load testing with JavaScript-based test scripts

Locust for Python-based load testing with flexible user behavior modeling

CI/CD Integration

Your test automation should trigger automatically on commits, pull requests, and deployments.

Jenkins for flexible pipeline configuration with broad plugin support

GitLab CI/CD for integrated source control and pipeline management

GitHub Actions for workflow-based automation tightly coupled to repositories

CircleCI for fast parallel test execution with cloud-native infrastructure

Azure DevOps for end-to-end pipeline management in Microsoft environments

Although aqua cloud is not a pure QA automation tool, it natively integrates with CI/CD solutions like Selenium, Jenkins, Ranorex, and others. So, with aqua, you can have excellent QA orchestration as well as automation capabilities, all in one environment.

Mocking and Service Virtualization

Use mocks to isolate third-party dependencies and reduce test fragility caused by external service instability.

WireMock for HTTP service virtualization with flexible request matching

Mockito for unit-level mocking within Java test suites

Mountebank for multi-protocol service virtualization across TCP and HTTP

Hoverfly for lightweight service virtualization with capture-and-replay support

AI-Assisted QA Tools

World Quality Report data shows most companies are still in early experimentation with GenAI in QA. Use AI carefully, with human oversight and traceability in place.

aqua cloud for AI-enabled test and requirement generation as well as enhanced traceability and better audit trails

Testim for AI-powered test authoring and self-healing test maintenance

Mabl for low-code test automation with built-in ML-based stability features

Functionize for natural language test creation with AI-driven execution

Applitools for visual validation and cross-browser visual regression testing

Best Practices for Fintech Test Automation

A test automation strategy only works if it’s maintainable, scalable, and trusted. Fintech teams face unique constraints: strict regulations, high-risk transactions, sensitive data, and third-party dependencies that behave unpredictably. Here’s how to build a test suite that lasts and delivers value over time.

Start with a layered testing approach. Your test pyramid should include many unit and API tests, strong integration and contract coverage, targeted E2E tests, security and performance checks, and limited UI regression tests. Don’t build hundreds of fragile UI tests and skip the foundation. According to NIST SP 800-218, secure software development practices should be integrated into SDLC models, which means testing is part of your security posture.

Prioritize based on risk. Automate the flows that carry the highest financial, security, or compliance risk first: money movement, authentication, KYC, card data handling, and admin permissions. A bug in a promotional banner is annoying. Payment flow bugs are regulatory incidents.

Use realistic but synthetic test data. Real customer data and payment credentials don’t belong in test environments. Generate synthetic datasets that mimic production behavior, covering users, accounts, transactions, cards, and KYC documents, but anonymize everything. Mask logs, scrub screenshots, and enforce strict access controls on test data.

Mock unstable third-party services. Payment gateways, bank APIs, and KYC providers fail, time out, or return unexpected responses. Use mocks and service virtualization to isolate these dependencies during testing. Run contract tests to verify API agreements, but don’t let third-party instability break your CI/CD pipeline.

Embed security testing in CI/CD. Don’t wait for annual penetration tests to catch security issues. Run SAST, SCA, secret scanning, container scanning, and DAST in your pipeline. Use OWASP standards as your baseline and treat security findings as blockers.

Define 2–3 non‑negotiable flows (e.g., sign‑up, KYC, money in/out) and treat them like a pre‑flight checklist before every deploy. Run those flows exactly the same way every time and capture them (screen + notes) so you can compare “what changed” between releases. Anything outside those flows is tested opportunistically or via automated checks when you have capacity.

Make tests auditable. Every automated test should produce evidence that links to a requirement, risk, or control. Test reports should show what was tested, when it ran, which environment it ran in, what data was used, and what passed or failed. This documentation becomes your compliance paper trail.

Limit UI test coverage. UI tests are slow, fragile, and expensive to maintain. Use them only for critical end-to-end journeys. Most fintech failures happen in business logic, APIs, integrations, and data layers, so focus your automation there.

Validate ledger logic directly. After a transaction, verify sender balance, recipient balance, fees, ledger entries, notifications, audit trails, and reconciliation status. Top-level UI checks won’t catch backend accounting inconsistencies.

Monitor and measure. Track automation coverage, test pass rate, flaky test count, test execution time, defect detection rate, mean time to detect, and regression prevention. Use these metrics to spot gaps, improve stability, and prove ROI to stakeholders.

Conclusion

Automated testing for fintech apps is how you prove that financial software is reliable, secure, and audit-ready. Every bug carries weight: failed transactions erode customer trust, compliance gaps invite regulatory scrutiny, and security holes expose sensitive data. The strongest fintech teams treat testing as governance. They layer unit, API, contract, and E2E tests, embed security checks into CI/CD, validate performance under realistic load, and generate traceable evidence for every release. AI tools support that process, but human oversight and structured test design keep it defensible. Ship software that survives scrutiny.

If you’ve made it this far, you already understand that automated testing for fintech is regulatory infrastructure. The question is whether your current tooling can handle the complexity: ledger validation, third-party mocks, compliance documentation, and much more. aqua cloud, an AI-powered test and requirement management platform, was designed for exactly these purposes. It brings manual and automated testing together in one platform, with every test run generating traceable evidence linked back to requirements and risks. The AI Copilot, powered by retrieval-augmented generation, generates test cases grounded in your actual compliance standards, API contracts, and security policies. The result is coverage that reflects real regulatory requirements and edge cases your team would otherwise miss. aqua supports DORA compliance, ISO 27001 certification, and flexible deployment for data residency requirements. With 10+ native automation integrations and the Capture integration, every test run produces video and screenshot evidence, giving you a complete audit trail ready to export on demand.

Achieve audit-ready fintech test automation with 100% traceability and domain-trained AI

What is the difference between component testing and unit testing?

Unit testing validates individual functions or methods in isolation, focusing on logic correctness. Component testing validates larger modules or components that may include multiple units working together, often with some integration behavior. In fintech, unit tests check fee calculations or date logic, while component tests validate a payment processing module that includes validation, calculation, and state management.

Who is responsible for performing component testing: developers or QA engineers?

Both can perform component testing, but it’s typically a shared responsibility. Developers write component tests as part of their development workflow, especially in test-driven or behavior-driven environments. QA engineers design test scenarios, validate coverage, and ensure that component tests align with requirements and risk areas. In fintech, collaboration matters because QA understands edge cases and compliance risks that developers might overlook.

Why are stubs and drivers used in component testing, and when are they necessary?

Stubs and drivers simulate dependencies when testing components in isolation. Stubs replace called modules, such as a payment gateway API, and drivers replace calling modules, such as a controller invoking the component. They’re necessary when testing a component before its dependencies are ready, when dependencies are unstable, or when you want to isolate failure modes. In fintech, stubs are common for mocking bank APIs or KYC providers during component tests.

Can component testing be fully automated, or does it still require manual effort?

Component testing can be largely automated, but it requires manual effort for test design, scenario selection, mock setup, and result validation. Automation handles execution and regression coverage, but humans define what to test and why. In fintech, manual effort is especially important for edge cases, compliance scenarios, and negative tests that require domain knowledge to design correctly.

Home » Alternative Tools » How to Automate Testing for Fintech Apps: Tools, Process & Strategy

Do you love testing as we do?

Join our community of enthusiastic experts! Get new posts from the aqua blog directly in your inbox. QA trends, community discussion overviews, insightful tips — you’ll love it!

We're committed to your privacy. Aqua uses the information you provide to us to contact you about our relevant content, products, and services. You may unsubscribe from these communications at any time. For more information, check out our Privacy policy.

X

🤖 Exciting new updates to aqua AI Assistant are now available! 🎉