Key Takeaways

- Insurance requirements management connects policy wording, rating engines, underwriting rules, and claims systems to prevent costly misalignments and regulatory breaches.

- Fragmented documentation across Word, Excel, Jira, and SharePoint creates approval bottlenecks, missed dependencies, and weak audit trails for regulators.

- Effective requirements management reduced one insurer’s pricing update timeline from six months to six weeks while maintaining compliance and consistency.

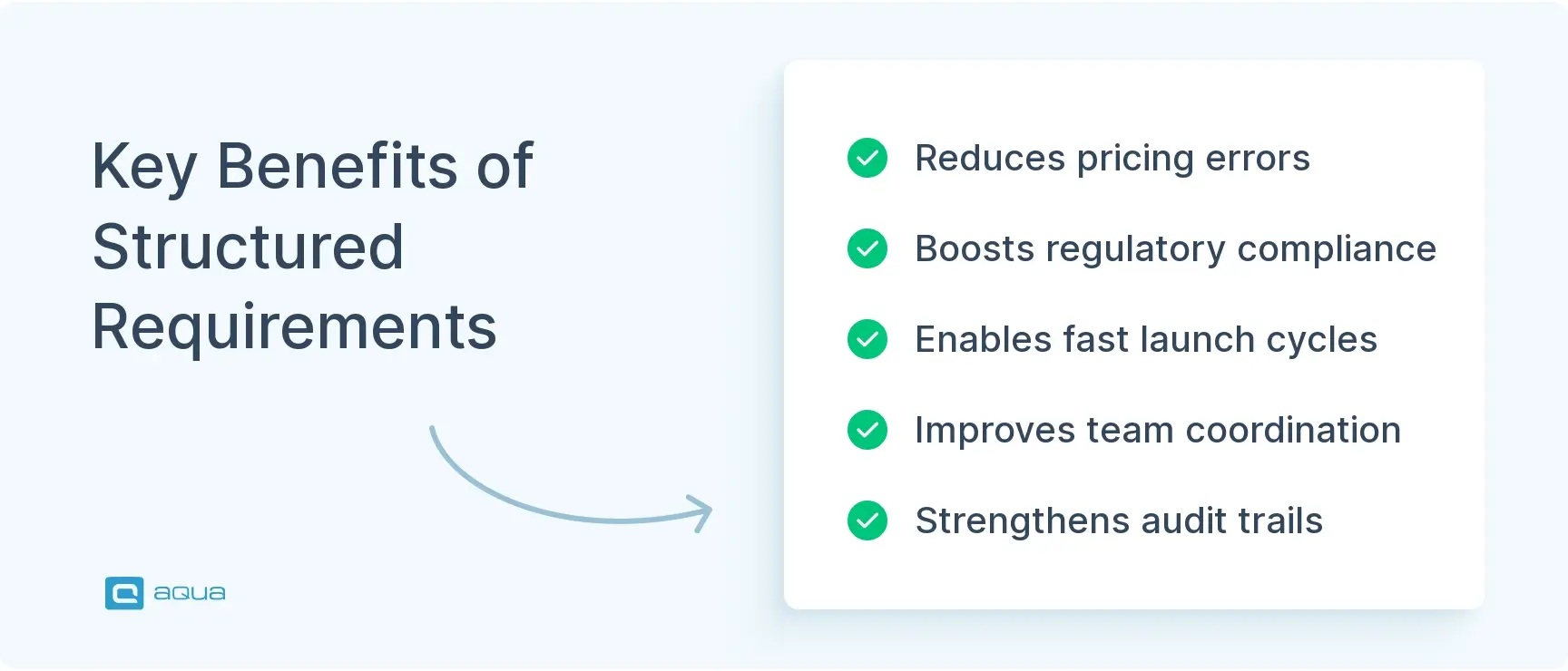

- The best practice is establishing a single source of truth with structured requirement IDs, clear ownership, approval workflows, and end-to-end traceability.

- Tools like aqua cloud, Jira, and Azure DevOps support insurance-specific requirements management by linking business rules directly to test cases and compliance evidence.

Discover how proper requirements management prevents pricing errors and other regulatory issues 👇

The Significance of Requirements Management in Insurance

Insurance products create downstream dependencies across more teams and systems than almost any other product type. That’s why requirements management here starts with evaluating how far a single requirement can reach.

One Requirement, Many Downstream Effects

Insurance products sit at the intersection of law and finance as well as operations and technology. A single product requirement can cascade across all of the following:

- Policy wording and coverage definitions

- Rating engines and pricing logic

- Underwriting eligibility rules

- Claims handling and evidence requirements

- Billing systems and payment logic

- Compliance filings and regulatory submissions

- Customer communication templates

Basically, any connection gets omitted or fails, and the entire procedure breaks down at once. And unlike with software, you can’t patch the entire workflow fast.

Why Post-Launch Errors Cost More in Insurance

Once you’ve issued a policy, you’re committed to that contract until renewal. This means that if your system calculates premiums differently from what you promise to your customers, you get a critical issue. What you’re dealing with is a potential regulatory breach and a customer harm scenario requiring full investigation and documentation.

Good requirements management acts as the connection point between what your actuaries model and what your legal team drafts. Those decisions connect directly to what engineers configure and what customers ultimately receive. When done well, coverage logic, pricing rules, underwriting decisions, and claims handling all reflect the same product intent. That alignment directly impacts launch itself and post-launch support and maintenance.

The Compounding Risk of Long-Lived Products

Insurance products are long-lived financial instruments, and the stakes stay high throughout their lifecycle. Changes to a single exclusion can affect:

- Rating logic and pricing models

- Reinsurance treaties and reporting

- Compliance filings across jurisdictions

- Customer-facing documents and templates

- Broker training materials

Without structured requirements management, your team is hoping that everyone interpreted a standard exclusion consistently across six different departments. Unfortunately, that doesn’t always work like that. Now, claims are declining cases that sales believed were covered.

As products mature and regulations shift, keeping everything synchronized requires discipline and clear ownership. A shared source of truth your whole team can reference is what makes both possible. So, you should prioritize establishing and maintaining one.

Insurance is a high-stakes domain where products intertwine legal and financial components as well as operations. That’s what makes requirements management here substantial. The fragmentation described here, with documents stored all across Word, Excel, and SharePoint, creates significant risk. This is where aqua cloud, an AI-powered test and requirements management solution, provides exceptional value for insurance businesses. With aqua, your team establishes a single source of truth, connecting policy wording, coverage rules, underwriting logic, and system behavior through end-to-end traceability. Its structured approach maintains clear ownership and approval workflows that satisfy regulators while enabling the scenario-based validation needed for complex insurance products. aqua’s domain-trained AI Copilot can automatically generate requirements and test cases directly from policy documents. The AI is grounded in your specific insurance context, ensuring outputs that reflect your product’s actual language and compliance needs. aqua cloud also integrates with Jira, Azure DevOps, GitHub, and GitLab, so your team can connect requirements management to your existing development and testing workflows.

Reduce regulatory risk and launch insurance products 40% faster with aqua

Challenges in Insurance Requirements Management

Requirement failures in insurance tend to follow recognizable patterns. Here’s where things typically break down, and what makes each failure mode worth understanding.

Fragmented Documentation Across Teams

The most common breakdown starts with documentation scattered across too many systems. Product teams use Word docs, actuaries work in Excel, legal drafts contracts using Track Changes, IT logs tickets in Jira, and compliance maintains checklists in SharePoint. When someone asks what the underwriting rule is for a specific coverage area, the answer is typically buried across seven files and multiple email threads. That’s before factoring in the institutional knowledge that walked out the door when someone resigned.

This fragmentation creates approval bottlenecks and missed dependencies, leaving a weak audit trail when regulators ask questions.

The Gap Between Business Language and Technical Specs

A second persistent problem is the gap between business language and technical specifications. Product managers describe customer outcomes and coverage intent, while engineers need exact field names, validation rules, and system workflows. For example, the product brief says “customers with recent claims should pay more.” Your rating engine interprets “recent” as 12 months and underwriting thinks it means 24 months, while the policy wording says 36 months.

Nobody catches the mismatch until post-launch testing reveals pricing inconsistencies that require manual fixes and potential premium recalculations.

Policy Wording Versus System Logic

This is the highest-risk divergence in insurance requirements management. The contract promises one thing; the system does another. Consider a policy that excludes claims for “pre-existing conditions diagnosed within 12 months,” while the claims system only checks conditions from the last 6 months. Valid claims get paid incorrectly, or worse, valid claims get denied. Both outcomes create customer harm and direct regulatory exposure. Reputational damage follows.

Product Changes Without Impact Analysis

Updating exclusion wording to clarify ambiguous language seems harmless, but that exclusion may also:

- Feed into the rating algorithm

- Trigger specific underwriting referrals

- Affect reinsurance reporting

- Appear in three different customer communication templates

When none of those downstream systems are updated, your product becomes internally inconsistent. And the main issue is that you won’t discover it until a complaint surfaces the gap, at which point the fix is expensive, and the regulatory explanation is uncomfortable.

Testing Disconnected From Requirements

QA teams verify that screens load and buttons work, but may not systematically validate business conditions. Can the system correctly calculate a premium for a 51-year-old homeowner in a flood zone with optional contents cover and a prior claim? If that requirement isn’t explicitly traced to a test case, the answer is probably not. And that’s just one of many possible concerns.

System changes then carry regression risk, because your team has no reliable way to confirm that specific business rules still work as intended. Without traceability from requirement to test, your team doesn’t have much control over releases.

For me, the toughest part of all RM tools I've used has been keeping the change history and rationale understandable to engineers who didn't write the original requirement. If a change occurs, we need to know why it happened and which tests or subsystems it touches without digging through pages of comments. That's where task tools just don't cut it.

BlueDolphinCute

Posted in

Reddit

Illustrative Use Cases of Effective Requirements Management in Insurance

The practical impact of structured requirements management shows up most clearly when teams face real product pressures. Here’s what it looks like across a pricing update, a compliance response, and a complex product launch.

1. Pricing Update Across Three Product Lines: Six Months to Six Weeks

Imagine a mid-market insurer needed to roll out a pricing change across three product lines in response to loss ratio pressure. Without proper requirements management, this would have been a six-month process involving missed rate changes and inconsistent documents, with regulatory filing errors to follow. Because the team maintained a structured requirements repository with traceability, they could immediately identify all rating rules and policy wording clauses the price change would touch. That visibility extended to document templates and underwriting referral thresholds, as well as all compliance filings that would need updating.

The update took six weeks and launched cleanly, passing regulatory review without objections. The difference was knowing exactly what needed to change before anyone wrote a single line of code.

2. FCA Fair Value Compliance: Identifying the Products That Didn't Qualify

A life insurer faced compliance-driven updates when FCA fair value rules tightened. The team needed to demonstrate that all non-investment products delivered fair value to their target market. Their requirements system linked product features, target market definitions, pricing assumptions, and distribution strategy. That connection let them rapidly generate evidence showing how products met the new standards.

Two outcomes followed:

- Products that met fair value criteria were evidenced quickly, with minimal manual reconstruction

- Two products that didn’t meet the criteria were identified and withdrawn before regulatory scrutiny intensified

That visibility prevented potential enforcement action, which would have been far more costly than the withdrawal process itself.

3. Cyber Insurance Launch: Cross-Functional Coordination Across Five Teams

A commercial insurer launching a cyber insurance product struggled with coordination across underwriting, pricing, legal, IT, and compliance. Underwriting needed security audit requirements while pricing sought claims history for rating factors. Legal was deep in exclusion wording negotiations with reinsurers, and IT was configuring the policy admin system. Compliance, meanwhile, was tracking state-level filing requirements across multiple jurisdictions.

Weekly requirements reviews gave the full team visibility into how their decisions affected the others. When underwriting added a new security control question, the effects were visible immediately:

- Pricing flagged the impact on rating logic

- IT identified the PAS configuration change required

- Legal noted the wording implication for the policy document

- Compliance confirmed no additional filing issues

The product launched on schedule with zero post-launch defects tied to requirement mismatches. These outcomes follow from treating requirements as the shared source of data your whole team works from.

Best Practices for Optimizing Requirements Management in the Insurance Industry

1. Establish a single source of truth

Before anything, your team can and most likely should keep their preferred tools. Actuaries can keep using Excel, and the legal department may proceed using Word, while IT may stay in Jira. What matters is having one system that holds the approved, versioned, traceable requirement that all other artifacts reference. When someone on your team needs the current rule for a specific coverage, the answer should point to a requirement ID. That ID should carry a clear owner, approval history, linked policy wording, and version control showing what changed and why.

2. Assign clear ownership to every requirement type

Most insurers have requirements floating with unclear accountability, where everyone assumes someone else is responsible. The result is that requirements drift until something breaks. Clear ownership looks like this:

- Product owns commercial requirements such as target market definition and customer value proposition

- Underwriting owns eligibility and referral rules

- Actuaries own pricing and rating logic

- Legal owns policy wording

- Compliance owns regulatory requirements

- Claims owns claims handling rules

- IT owns system behavior specifications

- QA owns test evidence

3. Implement end-to-end traceability

Take a requirement like “homeowners need protection against storm damage.” Good traceability means linking that requirement through coverage wording and underwriting eligibility, continuing through to rating factors and the test scenarios that validate them. When your team updates any part of that chain, traceability immediately flags what else needs review. This prevents the failure mode where policy wording gets updated, but the claims system configuration stays unchanged, creating a coverage promise your operations can’t deliver.

4. Use structured requirement IDs and taxonomy

Relying on document names or section numbers creates confusion as products get upgraded. Structured IDs make requirements searchable and auditable for anyone on your team. A practical taxonomy looks like this:

- PRD-027 for product requirements

- COV-014 for coverage requirements

- UND-033 for underwriting requirements

- RAT-019 for rating requirements

- CLM-008 for claims requirements

- REG-051 for regulatory requirements

The ID should carry a description, owner, source, priority, acceptance criteria, related requirement links, approval status, test coverage, and change history.

5. Build approval workflows that match your governance model

All significant requirements should pass through defined checkpoints: business case review, actuarial validation, legal approval, compliance check, IT feasibility, and operational readiness. The workflow should capture who approved what and when, with supporting evidence attached per decision. This creates an audit trail for regulators and supports root cause analysis when issues appear after launch.

6. Validate requirements through realistic scenarios

Confirming that the rating engine returns a number tells you very little. The real value comes from verifying it calculates correctly for a 45-year-old homeowner in a high-risk flood zone with optional contents cover and no prior claims. That level of specificity forces your team to work through actual business rules. It also creates regression test suites that protect product quality as systems improve.

So the requirements are all there, but they would need to be extracted to another system that would be a bit better suited for future, ongoing development. So that was one technical hurdle, but there are also political considerations here as well.

r/ExperiencedDevs

Posted in

Reddit

Best Tools for Insurance Requirements Management

The right tooling moves requirements management from a documentation burden to genuine product intelligence. Selecting the right platform starts with understanding what your team actually needs from a requirements system. Here’s what works in insurance environments:

aqua cloud is purpose-built for QA teams that need serious traceability and compliance evidence in one system, with test management built in. It connects requirements directly to test cases, tracks approval workflows, maintains version history, and generates audit reports that regulators accept. aqua cloud handles complex requirement dependencies across policy wording, pricing logic, underwriting rules, and claims handling. The structured evidence trail it creates supports both compliance and product velocity. It supports FCA PROD 4 and DORA compliance, as well as SERFF filing environments.

Jira works well for teams already in Atlassian ecosystems. Effective for tracking requirement changes and linking requirements to development tickets, with backlog prioritization built in. The challenge is keeping requirements structured and traceable, since they can dissolve into user stories with vague acceptance criteria over time. Another good thing about Jira, is that it can be natively integrated with aqua cloud.

Azure DevOps suits insurers on Microsoft infrastructure who need requirements, development, testing, and deployment in one platform. The work item tracking supports custom requirement templates, and integration with repos and pipelines helps maintain traceability from requirement through to release. This solution also has integration with aqua cloud’s platform.

Confluence works as a documentation hub for requirement specifications, policy wording drafts, and decision records. It functions well as a collaboration layer alongside dedicated tools, though it lacks the traceability and approval workflow features of a purpose-built requirements system. Confluence is another software that has an API-based integration with aqua cloud.

IBM DOORS suits insurers with deep regulatory obligations and complex product portfolios. It offers powerful traceability and baselining capabilities, with detailed change impact analysis included. The platform scales well for large organizations managing hundreds of products across multiple jurisdictions, though it’s more than most smaller teams need.

When evaluating an insurance product requirements management tool, focus on whether it supports traceability, approval workflows, version control, and test linkage. Those four capabilities separate genuine requirements management from documentation storage.

Effective requirements management helps notably with maintaining product integrity and regulatory compliance. aqua cloud, an AI-powered test and requirement management platform, directly addresses challenges caused by the complexity of the insurance domain. From establishing structured requirement IDs and taxonomies to managing approval workflows that match your governance model, aqua delivers the traceability insurers need. The platform connects requirements directly to test cases and maintains full version history. It generates compliance evidence that regulators accept. Its domain-trained AI Copilot, powered by RAG technology grounded in your actual project documentation, can automatically generate requirements documentation and test coverage. That alone saves up to 97% of manual effort, while keeping everything connected and audit-ready. For teams working within FCA PROD 4, DORA, or SERFF frameworks, aqua delivers both the speed and control required. aqua cloud integrates directly with Jira, Azure DevOps, GitHub, GitLab, and 12+ other tools from your tech stack.

Boost QA testing efficiency by 80% with aqua's AI

Conclusion

Requirements management connects business intent, policy wording, system behavior, and operational processes. A single product line is the most practical starting point. Structured requirements traced through to testing will show measurable impact on defect rates and launch timelines. The results make the case better than any methodology document. Your compliance team will appreciate the audit trail, and your product teams will appreciate the clarity.

{kind=link}