UAT in Banking: A Comprehensive Implementation Guide

Imagine your compliance team signed off, and the development team said the software was ready. Six weeks after go-live, a currency conversion module began rounding FX rates in the wrong direction. The error was small per transaction, yet resulted in thousands of operations being recorded incorrectly. This is one of many possible scenarios that can happen if User Acceptance Testing (UAT) is critically neglected. This guide covers how to run UAT properly, including the main UAT phases, common challenges, and best QA execution practices.

User Acceptance Testing in banking validates that systems perform correctly under real operational conditions with actual business users. Developers and QA engineers have completed their work before this stage begins.

Banking UAT focuses on financial accuracy, regulatory compliance, integration behavior, and operational readiness. Technical functionality is a baseline, not a finish line.

The UAT process includes requirement review, planning, test scenario creation, data preparation, execution, defect management, regression testing, and formal sign-off from stakeholders.

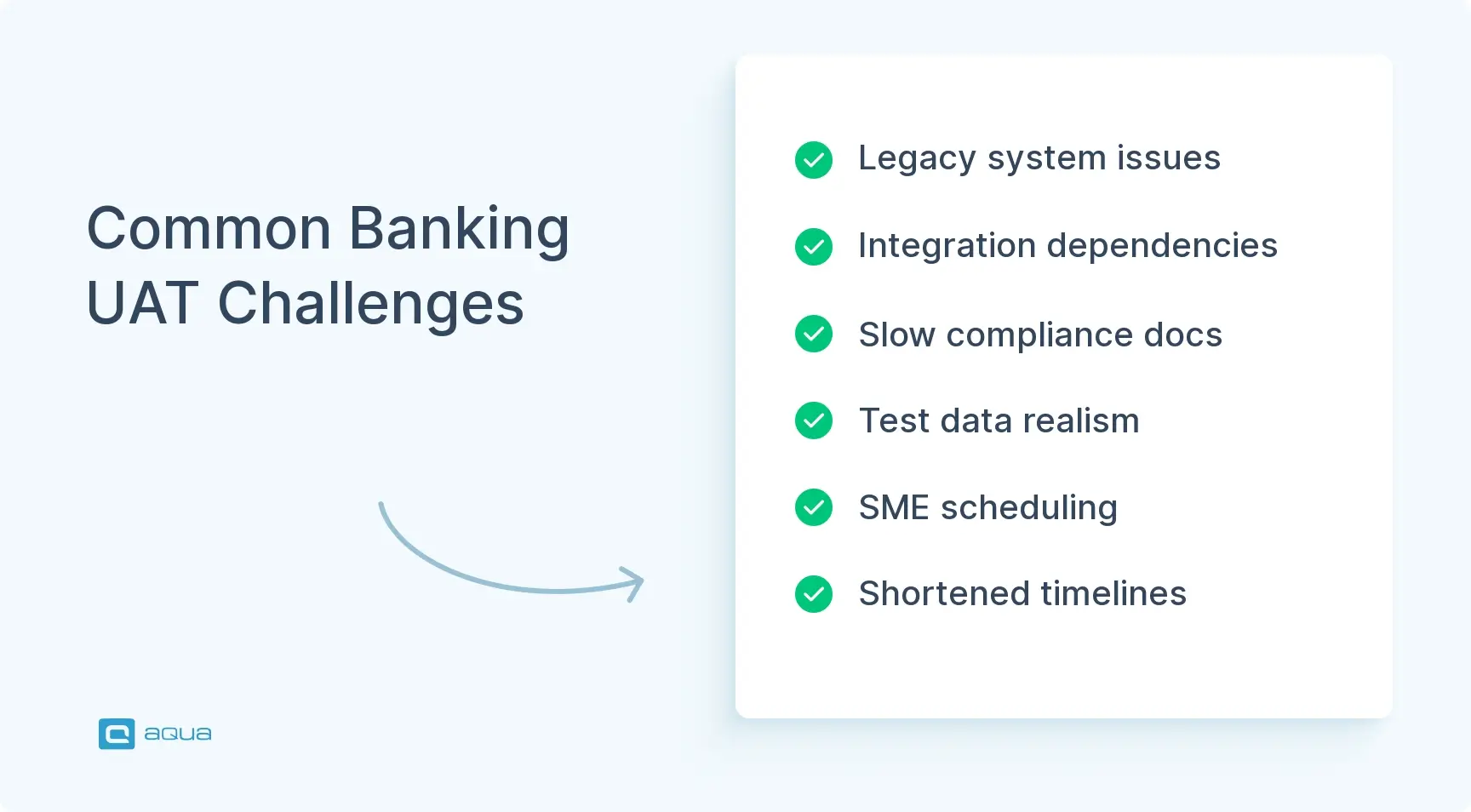

Common challenges include complex legacy systems, high integration dependencies, regulatory pressure, limited test environments, poor test data, and compressed timelines.

This guide shows how to implement effective UAT for your banking applications 👇

What is User Acceptance Testing (UAT) in the Banking Sector?

User acceptance testing in banking is the validation phase where users confirm that a system performs correctly under different operational conditions. Basically, UAT covers the concern of running banking procedures without exposing the institution to financial, regulatory, or customer risks.

A defect that clears earlier testing stages can trigger duplicate transfers or AML violations the moment it reaches production. That gap is why UAT in banking differs from System Integration Testing. SIT examines how technical components interact: APIs, databases, and message queues. UAT meaning in banking is different. Your UAT team spans operations and compliance roles alongside product owners, and may extend to customer representatives depending on scope.

Key characteristics of banking UAT:

Business process validation: Workflows like account opening, loan disbursement, or fraud escalation function as designed

Regulatory compliance checks: KYC, AML monitoring, GDPR controls, and audit logging meet legal standards

Financial accuracy verification: Interest calculations, FX conversions, fee logic, and repayment schedules compute correctly

Integration behavior testing: Connections to core banking systems, CRM platforms, SWIFT networks, and card processors work reliably

Operational readiness: Whether support and reconciliation teams can actually run the process when it goes live

Why UAT is Critical for Banking Applications

In most software projects, a post-release bug is an inconvenience that can be fixed without much trouble, unless it affects customers’ data. In banking, that same bug becomes a compliance incident. The paper trail can follow your organization for years. That is why UAT carries so much weight before any release.

A failed payroll batch or duplicate transfer creates immediate support and reconciliation work. When money moves incorrectly, customers lose funds and demand answers fast.

Regulatory non-compliance has no easy fix. Banks operate under PSD2, GDPR, Basel, and AML rules. A violation can result in fines, license suspensions, or forced rollbacks.

Broken onboarding flows and failed password resets push customers to competitors. A bank’s reputation takes years to build and weeks to lose.

Payment dependencies cause chain failures across downstream systems. One integration failure blocks entire workflows. Root cause analysis in production costs far more than catching the issue before release.

Support and reconciliation teams often find process gaps only during live incidents. UAT is the right time to surface those gaps, not after go-live.

Sign-off documentation becomes part of the audit record. Banks with thorough UAT evidence spend less time under regulatory scrutiny.

As you build your UAT framework for banking applications, you need an all-in-one testing environment for your procedures and documentation. aqua cloud, an AI-powered test and requirement management platform, offers a purpose-built solution for banking UAT. With comprehensive test case management for complex banking workflows, aqua enables you to establish complete traceability from requirements to test execution. This assistance is essential for demonstrating regulatory compliance during audits. aqua’s domain-trained AI Copilot can automatically generate relevant test scenarios for banking processes like payment processing and KYC verification. This can reduce UAT preparation time by up to 43% while maintaining high quality standards. aqua also connects natively with Jira, Jenkins, Azure DevOps, Confluence, and 12+ additional automation tools. This way, your UAT process fits directly into the development infrastructure your team already uses.

Achieve 100% traceability and maintain bank-grade compliance standards

Banking UAT follows a structured sequence. Teams usually discover missing requirement alignment during execution, when SMEs are already booked into testing sessions, and re-planning creates delays across the board.

Requirement review. Business stakeholders examine requirements, regulatory obligations, process flows, and acceptance criteria before any scenario is created. This alignment step is where QA leads and compliance groups need to be in the same room.

UAT planning. Scope, timelines, entry and exit criteria, test environments, roles, and escalation processes all get defined here. Key deliverables include a UAT test plan, scope document, test schedule, and defect management protocol.

Test scenario creation. Scenarios must reflect real banking workflows: opening current accounts, processing SWIFT payments, rejecting high-risk customers, reversing failed transfers. Scenarios built only around the expected flow consistently miss the failures that matter most.

Test data preparation. Banking UAT datasets should mirror production behavior closely enough to expose reconciliation and compliance failures. This means masked datasets covering customer profiles, account balances, payment histories, AML flags, and multi-currency accounts.

UAT execution. Business users run scenarios and record outcomes across workflow correctness, financial accuracy, compliance controls, and exception handling. The quality of this phase depends on who runs it and how much dedicated time was protected.

Defect management. Defects get tracked, prioritized (critical, high, medium, or low), and retested after fixes. Broken compliance controls or incorrect financial calculations hold up release approval until resolved.

Regression testing. After fixes ship, regression testing confirms existing functionality still holds and that nothing broke in adjacent areas.

Sign-off. Business owners formally approve release readiness. Sign-offs come from product owners, operations leads, compliance officers, and IT leadership.

Good QA should look at anything they test from UAT perspective it's true. When you see the button and it's all small and hard to click do you report that? You should. That doesn't mean having an actual user look at it isn't helpful though.

UAT Process for Banking Applications (Step-by-Step)

The phases define the structure. What follows describes what actually happens at each stage and where the process breaks down most often.

Step 1: Entry criteria validation. UAT should begin only once development is complete, SIT has passed, the environment is stable, test data is loaded, and business users are scheduled. Starting before these conditions are met means SMEs spend their allocated time on QA environment issues instead of testing.

Step 2: Acceptance criteria definition. Document what a passing result looks like: transaction outcomes, balance updates, audit log entries, and regulatory reporting compliance. Vague criteria make sign-off conversations contentious and give auditors room to question the process.

Step 3: UAT team assembly. Include subject matter experts from operations, compliance, risk, and customer service. QA leads working without domain input miss edge cases that only become visible once real banking scenarios are in play.

Step 4: Test scenario development. Cover core workflows, edge cases, negative tests, and integration points: loan origination, card freeze and unfreeze, international transfers, AML alert escalation, and duplicate payment prevention.

Step 5: Test data preparation. The dataset should reflect a realistic cross-section: different account types, currencies, customer risk profiles, and product configurations. The closer it mirrors production, the more reliable the findings.

Step 6: Execution. Business users run scenarios, record outcomes, and flag discrepancies. Workflow accuracy, compliance controls, and financial calculations all need verification here.

Step 7: Defect logging. Log issues with clear descriptions, reproduction steps, severity assessments, and screenshots. Incomplete defect records create ambiguity during sign-off and resurface as compliance questions later.

Step 8: Fix retesting. After the development team addresses defects, affected scenarios get retested alongside regression checks.

Step 9: Final validation sweep. Once critical and high-priority defects are resolved, run a final pass across all in-scope scenarios to confirm acceptance criteria are met.

Step 10: Formal sign-off. Stakeholders provide documented approvals confirming release readiness. In UAT in agile environments and waterfall alike, this documentation is an audit artifact.

Common Challenges in Banking UAT

Banking UAT is more demanding than UAT in most other industries. The key UAT challenges and solutions vary by organization, but these seven appear consistently across banking environments regardless of team size or stack.

1. Legacy systems often behave in ways nobody documented. Behavior lives in undocumented integrations, and testing frequently uncovers it mid-cycle when there is no time to re-plan.

Mitigation strategy: Assign a dedicated SME for legacy integrations before UAT begins. Document known undocumented behaviors in advance and budget extra time for discovery during execution.

2. Payment dependencies create chain failures across downstream systems. When one integration goes down, it blocks everything connected to it, and the delay ripples across the release schedule.

Mitigation strategy: Use service virtualization or API mocking for unavailable integrations. Map all dependencies upfront and establish escalation paths before execution begins.

3. Compliance documentation slows execution more than most teams estimate during planning. Every test must trace back to a requirement, a regulation, or a risk assessment, and that overhead compounds across large test suites.

Mitigation strategy: Build requirement-to-test traceability into your test management tool, such as aqua cloud, an AI-driven platform, from day one. Automated linking reduces documentation overhead significantly compared to manual tracking approaches.

4. UAT environments frequently diverge from production in ways that only matter at go-live. Missing integrations and unstable configurations create blind spots that testing cannot catch.

Mitigation strategy: Run an environment parity audit before UAT planning is complete. Document every known gap and assess whether it requires a compensating control or workaround.

5. Unrealistic test data produces results that look fine but predict nothing. If the dataset does not reflect what production actually sees, the findings are not reliable.

Mitigation strategy: Establish a dedicated test data management process using a trustworthy test and requirement management platform like aqua cloud. Many teams report fewer environment-related failures after introducing masked production datasets validated against current transaction patterns.

6. Scheduling subject matter experts is a persistent bottleneck. These are the people with the domain knowledge UAT depends on, and they are usually already fully committed to operational work.

Mitigation strategy: Secure formal time commitments from SMEs before UAT planning is finalized. Treat their availability as a fixed constraint in the project schedule, not a best-effort agreement.

7. When deadlines compress, UAT is the first phase to get shortened. Shallow coverage follows, and defects that would have been caught reach production.

Mitigation strategy: Define minimum UAT scope and exit criteria in advance. When pressure builds, de-scope low-risk scenarios rather than reducing depth across critical-path testing.

UAT can also be a test environment for customers who are integrating with the system. If you're adding a feature or modifying an existing API, UAT can be a place for customers to test against…

These practices address both QA leads designing the testing process and C-level stakeholders deciding how much time and resource UAT deserves. Each one comes with a way to measure whether your team is actually following it.

Test data coverage determines whether results mean anything. Banking UAT datasets should cover at least 85% of the transaction types your system handles in production. Teams testing with a small number of customer profiles miss the edge cases that drive the majority of post-release defects in core banking systems. A practical benchmark: if your UAT data does not cover the top error scenarios your support team handled last quarter, there is a coverage gap worth addressing before execution begins.

Risk-based prioritization is a resource allocation decision, not a testing preference. Most banking teams prioritize workflows using three factors: transaction exposure, compliance impact, and failure frequency in past production incidents. High-risk scenarios should receive the majority of your UAT time budget. This keeps effort concentrated where exposure is highest, which matters most when timelines compress near release.

Defect Detection Efficiency is the metric leadership should be tracking. Banking UAT should aim for a Defect Detection Efficiency above 85% before any release. The formula: DDE = (Defects found in UAT / Total defects in UAT and production combined) x 100. QA leads tracking this number across releases will notice patterns: teams below 75% DDE usually have shallow test coverage, insufficient business user involvement, or both.

Linked requirements, defects, approvals, and execution history are what auditors look for. Every test case should map to at least one requirement or regulatory obligation. Organizations with less than 90% traceability coverage spend significantly more time on manual documentation reconstruction during audits, which delays regulatory responses and creates avoidable exposure.

Failure scenarios belong in your test plan by design. AML hits, insufficient funds, expired cards, and system timeouts are routine conditions in banking, not edge cases. Release managers who track the ratio of failure scenarios to total test cases will often find it is lower than it should be. A target of at least 30% failure scenarios per release cycle is a reasonable starting point.

Business user involvement rate is a leading indicator of post-release stability. Aim for 70% or more of UAT execution performed by actual business users. QA teams working without enough domain involvement miss regulatory nuances and process realities that compliance groups and operations staff catch without being prompted.

Incomplete sign-off documentation extends regulatory inquiry timelines. Organizations without written approvals from all required stakeholders spend more time in regulatory inquiries when post-release incidents occur. The evidentiary record is what regulators examine first, and gaps in it become the focus of the inquiry.

For a broader look at available options, explore the best UAT tools for testing management.

Tools for UAT in Banking

The toolset your team uses affects how efficiently UAT runs and how well the outputs hold up under regulatory scrutiny.

aqua cloud: Built for high-compliance UAT in regulated environments. The domain-trained AI Copilot generates test scenarios from requirements, including regulatory documents and user stories, cutting UAT preparation time meaningfully. The traceability matrix links every test case to specific requirements and compliance controls automatically. Bidirectional Jira synchronization means QA teams work in aqua while developers stay in Jira, with changes reflected in both directions without manual re-entry. Defect management, approval workflows, and nested test scenario reuse across different banking products all live in the same environment. Regulated European banks, as well as other financial or government institutions use aqua to meet strict regulatory documentation requirements while keeping UAT processes manageable at scale.

Save 12.8 hours per tester per week with aqua’s AI.

Save 12.8 hours per tester per week with aqua's AI

JIRA: Widely used for defect tracking and cross-team collaboration. Banking teams configure custom workflows that mirror their approval processes and compliance requirements.

HP ALM / Micro Focus ALM: Connects requirements to tests to defects. Common in large banks that need linked requirements, defects, approvals, and execution history for audit purposes.

Confluence: Used alongside Jira to maintain UAT plans, test scenarios, acceptance criteria, and sign-off records.

Selenium / Playwright: Regression testing frameworks that help QA teams validate that fixes did not break existing functionality between test cycles.

Postman / ReadyAPI: API testing tools for validating integration behavior and backend workflows, increasingly relevant as open banking architectures expand.

Tosca: Model-based test automation for functional and regression testing. Some banking teams use it to automate repetitive scenarios while keeping business-critical tests manual.

aqua cloud integrates natively with Jira, Jenkins, Azure DevOps, Confluence, SoapUI, Ranorex, and several other tools listed above. QA teams keep their existing workflows intact while gaining a dedicated UAT management layer built for the compliance demands of regulated banking environments.

UAT Checklist for Banking Applications

Use the table below to track readiness across your release. Priority levels reflect the regulatory and financial exposure associated with each area.

#

Area

What It Covers

Owner

Priority

1

Entry criteria

Development complete, SIT passed, environment stable, test data loaded, users scheduled

Test Lead

Critical

2

Test scenario coverage

All requirements mapped, negative cases included, integration points covered

Monitoring tools, manual processes, escalation workflows, SME readiness

Operations Lead

High

10

Formal sign-off

Written approvals from product owners, operations leads, compliance officers, IT leadership

Project Manager

Critical

Banking UAT does not have to be a resource-intensive process. The right AI-driven test and requirement management platform, like aqua cloud, can make all the difference. aqua offers a solution that addresses the unique demands of banking applications with features specifically designed for financial UAT workflows. Its traceability matrix ensures your team’s tests link directly to requirements and compliance controls, creating audit-ready documentation that satisfies strict regulatory requirements. The platform’s domain-trained AI Copilot, which learns from your project’s own banking documentation, accelerates test creation while maintaining contextual relevance to your specific financial products and compliance needs. With nested test scenarios for reusability across different banking products and customizable approval workflows that mirror your sign-off processes, aqua helps your team deliver higher-quality releases faster. Leading financial institutions enhance risk management with aqua through native integrations with Jira, Jenkins, Azure DevOps, Confluence, and 12+ additional tools.

Boost the efficiency of your banking UAT QA by 80% with aqua cloud

Banking UAT is the control point that stands between a clean release and a production failure that costs money, reputation, or regulatory standing. Financial accuracy, compliance, and whether support and reconciliation teams can actually run the process all depend on testing that reflects real-world banking complexity. As banking systems grow more digital and API-driven, UAT demands will grow with them. Organizations that enforce strong governance, use production-like test data, and formalize approval processes reduce production incidents and maintain compliance. The goal is systems that work reliably when real money and real customers are on the line.

UAT testing in banking is the final validation phase where business users confirm that a system performs correctly under real operational conditions. It covers financial accuracy and end-to-end workflow validation, including regulatory compliance, before any production deployment.

What does UAT stand for in finance?

UAT stands for User Acceptance Testing. In finance, it is the process where business stakeholders validate that a system meets operational requirements before release, covering payment processing accuracy and compliance with regulatory controls.

How can UAT help improve customer experience in banking applications?

UAT validates customer-facing journeys like account opening and fund transfers before launch. Catching broken workflows and navigation failures during testing reduces the service disruptions and customer complaints that follow a poorly validated release.

What are common challenges faced during UAT in banking projects?

Common challenges include limited test environment stability, poor test data quality, compressed timelines near release deadlines, difficulty scheduling business users, and high integration dependency across core banking, payment, and compliance systems.

Home » Best practices » UAT in Banking: A Comprehensive Implementation Guide

Do you love testing as we do?

Join our community of enthusiastic experts! Get new posts from the aqua blog directly in your inbox. QA trends, community discussion overviews, insightful tips — you’ll love it!

We're committed to your privacy. Aqua uses the information you provide to us to contact you about our relevant content, products, and services. You may unsubscribe from these communications at any time. For more information, check out our Privacy policy.

X

🤖 Exciting new updates to aqua AI Assistant are now available! 🎉

{kind=link}